Third-quarter financial development was revised up 0.3 share level to three.5 % at an annual fee, the quickest quarterly development since 2014. The U.S. economic system is now 11.6 % bigger than its pre-crisis peak in 2007 amid its sturdy restoration because the worst financial disaster because the Nice Melancholy. Rising incomes, improved family steadiness sheets, and excessive ranges of shopper confidence have supported strong shopper spending development over the restoration. In the meantime, the housing sector has continued to get better from the disaster and exhibits additional potential for growth. Nonetheless, financial development has confronted quite a lot of headwinds within the present restoration, together with contractions in State and native authorities spending, weak international development (which has weighed on each exports and funding), and the demographic results of the getting older U.S. inhabitants. Extra work stays to additional strengthen development and to make sure that it’s broadly shared, together with promoting greater competition throughout the economic system; supporting innovation; increasing investments in infrastructure; and opening new markets to U.S. exports.

SEVEN KEY POINTS ON MACROECONOMIC PROGRESS OVER THE LAST EIGHT YEARS

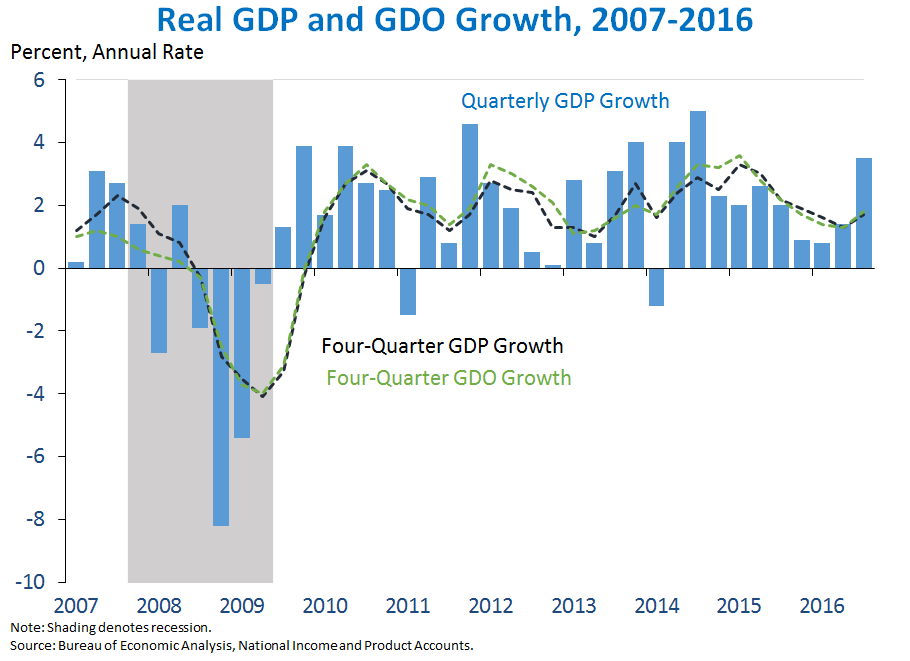

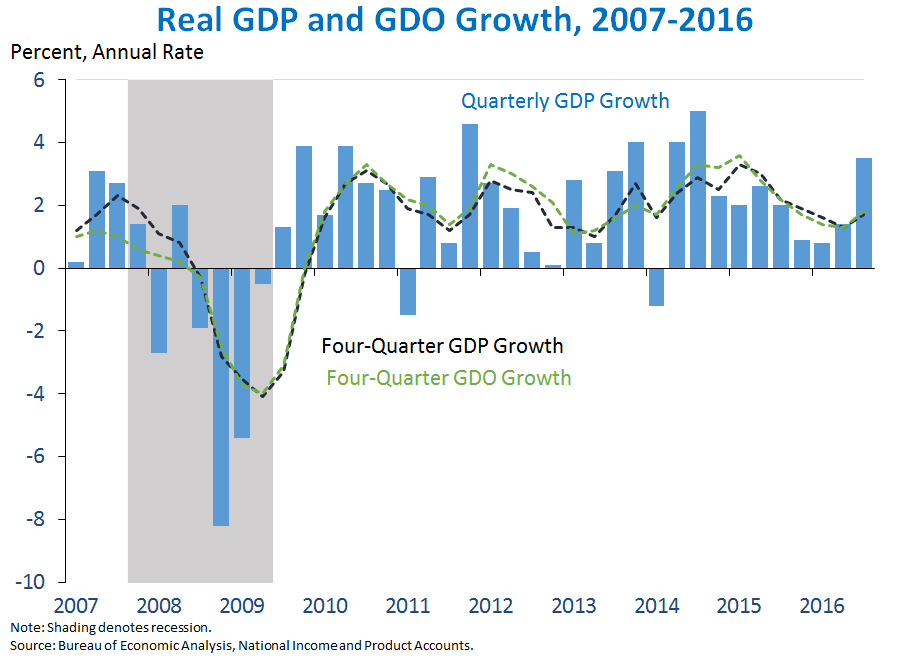

1. Based on BEA’s third estimate, actual gross home product (GDP) elevated 3.5 % at an annual fee within the third quarter of 2016, an upward revision of 0.3 share level (p.p.) from the second estimate. Actual shopper spending grew a powerful 3.0 % within the third quarter following strong development within the second quarter. Stock funding—one of many most volatile parts of GDP—added 0.5 share level to GDP development within the third quarter after subtracting 1.2 share factors within the second quarter. Residential funding declined for the second quarter in a row, although at a slower tempo within the third quarter than within the second. Notably, exports grew 10.0 % at an annual fee within the third quarter, their quickest quarterly development since late 2013, boosted by a possible transitory leap in agricultural exports.

Actual gross home revenue (GDI)—an alternate measure of output—elevated 4.8 % at an annual fee within the third quarter. (In principle, GDP and GDI must be equal, however in apply they often differ as a result of they use totally different information sources and strategies.) The typical of actual GDP and actual GDI, which CEA refers to as actual gross home output (GDO), elevated 4.1 % at an annual fee within the third quarter. CEA analysis means that GDO is a better measure of financial exercise than GDP (although not usually stronger or weaker).

The 0.3-p.p. upward revision to GDP development was greater than accounted for by upward revisions to shopper spending, enterprise mounted funding, and State and native authorities spending. Nonetheless, the general contour of third-quarter development was largely unchanged from final month’s second estimate.

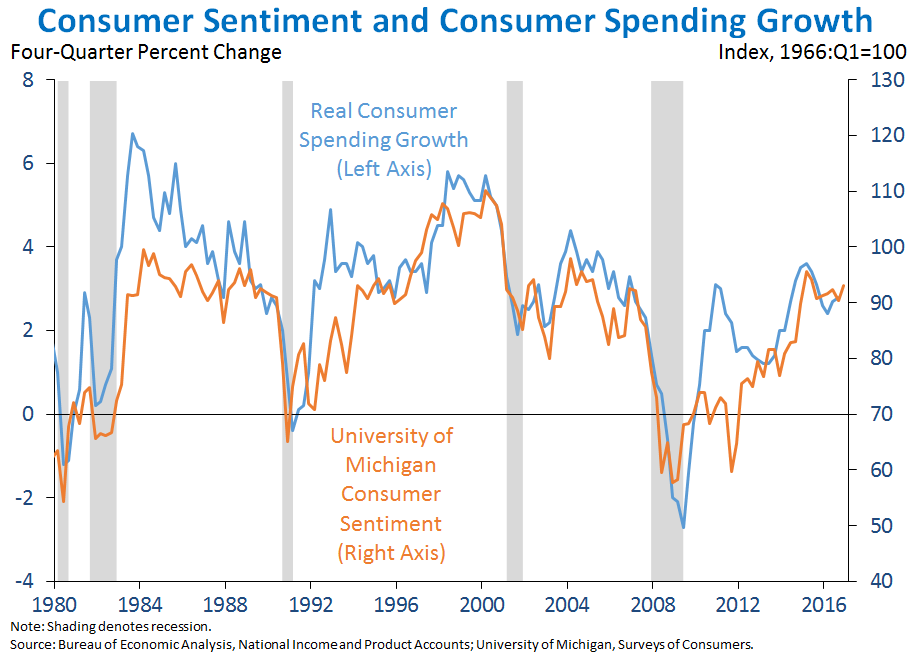

2. Robust shopper spending development over the present restoration has been supported by development in actual incomes, enhancements in family steadiness sheets, and excessive ranges of shopper confidence. Shopper spending accounts for over two-thirds of GDP, and has contributed disproportionately to total actual GDP development in recent times. This power in home demand displays improved financial situations for American households throughout a variety of measures. Actual wages have grown quicker over the present enterprise cycle than in any because the early Seventies (measured peak to peak), and from 2014 to 2015 actual median family revenue elevated 5.2 %, the fastest growth on record. In the meantime, as a share of disposable revenue, family debt service—the quantity that households should spend on curiosity and principal funds for his or her excellent debt—has fallen sharply in recent times, pushed each by low rates of interest and by sharp reductions in excellent family debt relative to revenue. Taken collectively, these components have left households with extra disposable revenue out there for shopper purchases. Lastly, customers have been more and more assured in recent times. Because the chart under exhibits, the College of Michigan index of shopper sentiment—which tends to intently monitor actual shopper spending development—is near its highest degree in ten years.

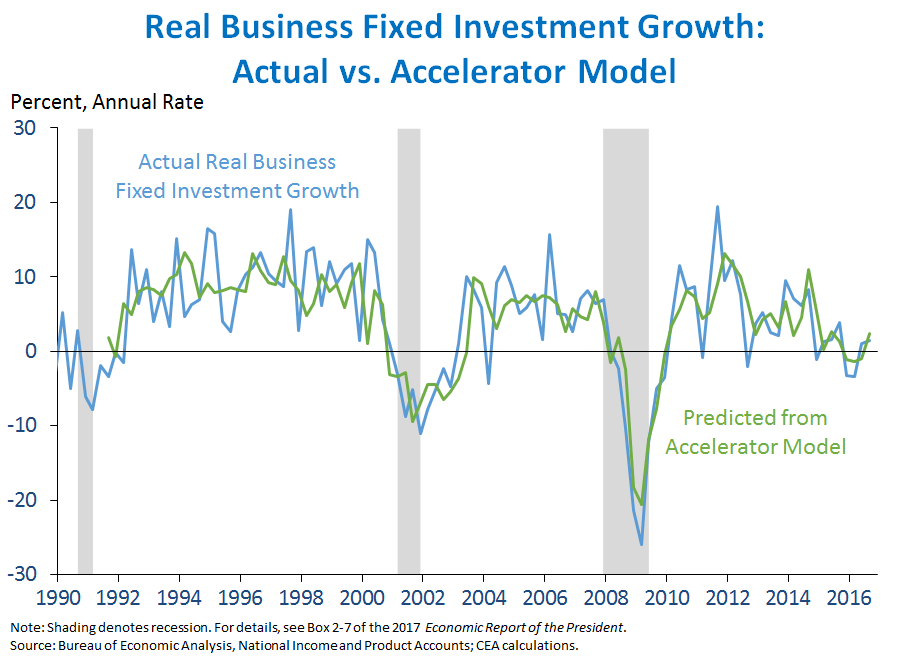

3. The latest slowdown in actual enterprise mounted funding development might be defined largely by modifications within the fee of U.S. and international GDP development, as mentioned in Chapter 2 of the 2017 Economic Report of the President. Whereas enterprise mounted funding—non-public spending on constructions and gear, in addition to expenditures on mental property merchandise resembling software program and analysis and growth (R&D)—constitutes simply 12 % of GDP, it’s essential to long-run development as a result of it offers employees with extra capital and improves expertise, thus contributing to productiveness development. Enterprise mounted funding development has slowed since 2014; whereas oil-related funding has dragged on total funding development on account of low oil costs, non-oil associated funding development has slowed considerably as nicely. CEA analysis finds that a lot of the slowdown in funding development might be defined utilizing an “accelerator mannequin,” which assumes that companies make investments in the event that they count on rising demand development for his or her merchandise, which means that rising GDP development charges will result in quicker funding development. The evaluation additionally finds that a number of components which have traditionally impacted funding development—together with credit score constraints and different monetary stress—have little explanatory energy in understanding the latest slowdown. Nonetheless, as a result of the mannequin predicts that funding follows modifications within the fee of GDP development, it predicts a rebound sooner or later, since U.S. and world output development are anticipated to stabilize or choose up barely within the years forward.

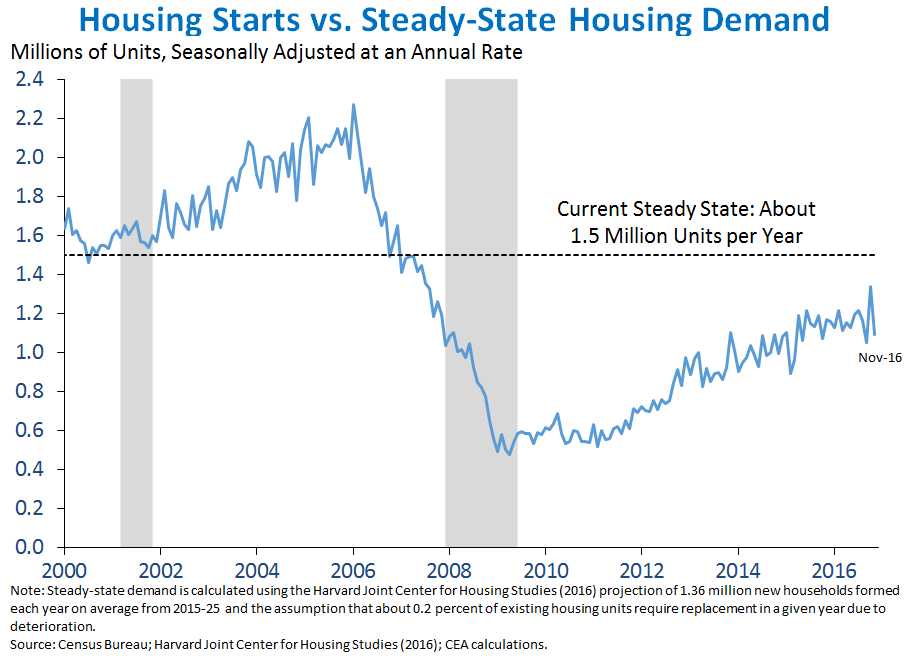

4. Ten years after the primary indicators of decline within the U.S. housing market, housing exercise and funding have step by step recovered, with room for future growth. Restoration within the housing sector has been supported by sturdy job development, rising actual wages, and low mortgage charges, with development in actual residential funding outpacing total actual GDP development over the course of the restoration from the Nice Recession. Even with the stable development in recent times, there may be room for additional growth in residential building. Because the chart under exhibits, housing begins stay nicely under the extent wanted to maintain tempo with inhabitants development, family formation, and typical charges of housing inventory substitute. CEA evaluation means that extra housing provide from overbuilding through the 2000s has been greater than offset by underbuilding in recent times. Low family formation, notably amongst younger adults, could also be taking part in a task in decreasing demand for housing. On the availability facet, local barriers to housing development in high-demand areas might also be one issue holding again new residential building. Nonetheless, residential funding has additional room to develop in future quarters, presenting upside potential for home demand within the near-to-medium time period.

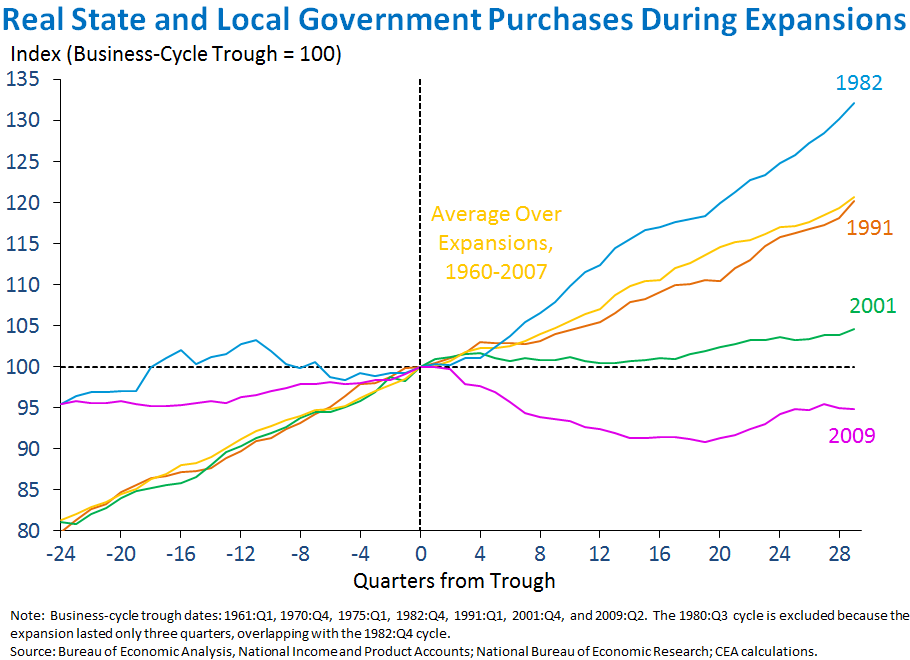

5. Traits in real State and local government purchases have differed sharply from prior enterprise cycles, with significant contractions amid budgetary cuts. Though in a typical restoration State and native spending tends to develop shortly and at an analogous tempo as within the pre-recession interval, State and native spending contracted sharply within the present enterprise cycle and, after seven years, has nonetheless not rebounded to its pre-crisis ranges. Through the 4 quarters of 2010, State and native purchases subtracted 0.5 share level from GDP development after which subtracted about one other 0.3 share level in each 2011 and 2012. Spending on this sector stabilized in 2013, added modestly to GDP development through the 4 quarters of 2014 and 2015, and had a negligible influence on GDP through the first three quarters of 2016. Actual State and native authorities purchases, in addition to State and native authorities employment, stay under their respective pre-crisis ranges. If State and native authorities purchases had elevated on the common fee of expansions excluding the present cycle (as proven within the chart under), actual GDP development would have been roughly 0.4 share level quicker per 12 months on common within the present restoration. Due partly to contractions in State and native authorities spending, complete actual authorities purchases are under their degree on the enterprise cycle peak in 2007; in different phrases, all the development in actual GDP within the present enterprise cycle is attributable to the non-public sector.

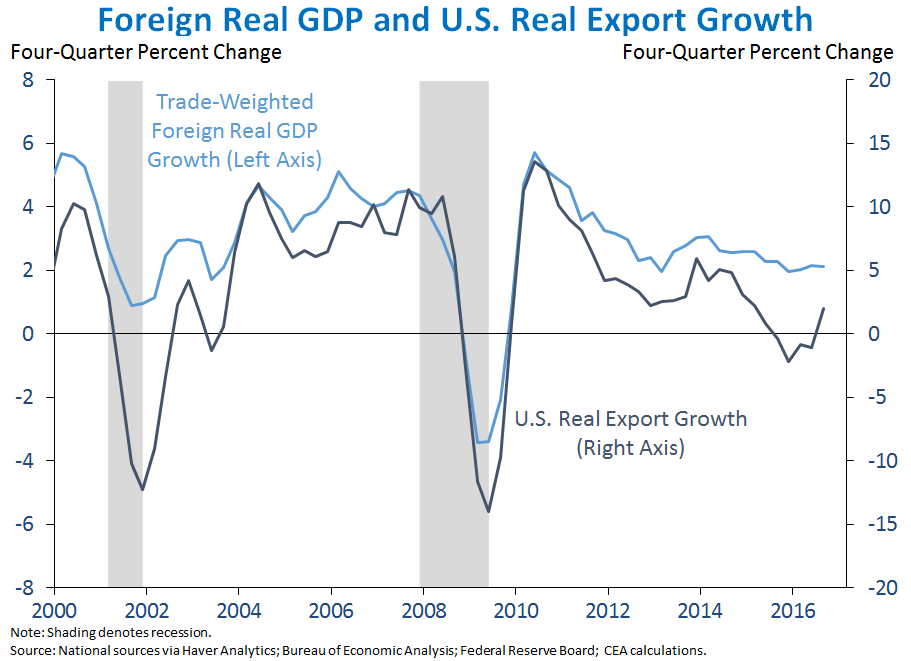

6. Progress in U.S. exports intently tracks world demand, with slowing world development creating key headwinds to U.S. development in recent times. The quantity of U.S. exports to international nations is delicate to international GDP development, and, as proven within the chart under, four-quarter international GDP development—when weighting nations by their relative significance to U.S. commerce—explains a lot of the variance in U.S. export development. Over the past 5 years, world development has persistently underperformed relative to forecasts, and in its October World Economic Outlook, the Worldwide Financial Fund (IMF) revised down its forecast of world development for the 4 quarters of 2016. Nonetheless, the IMF at present forecasts world development to select up in 2017, suggesting much less downward strain on U.S. export development—and on the manufacturing sector, which tends to be extra export-oriented than different industries—from weak international demand going ahead.

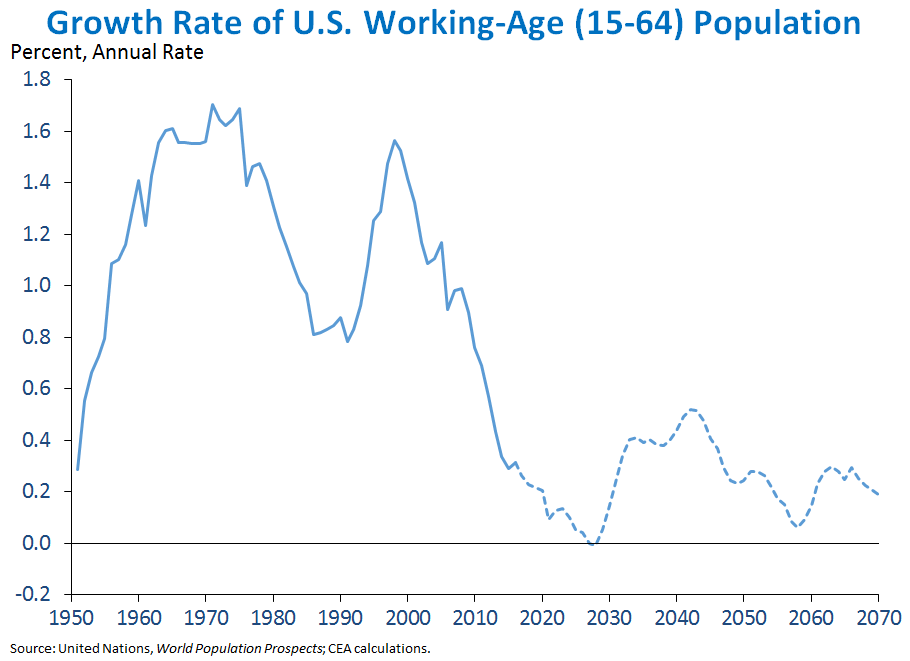

7. The aging of the U.S. population, a development that may proceed within the coming years, has positioned constraints on development in potential actual GDP. The expansion of the working-age (15-64) inhabitants in the US has slowed notably in latest many years, placing downward strain on labor drive participation and actual GDP development. The working-age inhabitants grew 1.4 % at an annual fee within the Nineteen Sixties via the Nineteen Eighties, however simply 0.6 % through the present enterprise cycle. (The speed of development of the prime-age [25-54] inhabitants has declined much more steeply, and the prime-age inhabitants even contracted between 2012 and 2015.) The decline within the development fee of the working-age inhabitants is anticipated to proceed via 2028, suggesting continued demographic headwinds to total development for not less than the subsequent decade. As famous in Chapter 2 of the 2017 Economic Report of the President, analysis has discovered that demographic shifts in direction of an older workforce could have additionally lowered productiveness development in recent times, although projections of the composition of the labor drive recommend that the drag on productiveness from demographics could quickly abate. Nonetheless, slowing productiveness development stays a key structural challenge that the US shares with all different main superior economies.

Because the Administration stresses each quarter, GDP figures might be unstable and are topic to substantial revision. Subsequently, it is vital to not learn an excessive amount of into any single report, and it’s informative to think about every report within the context of different information as they change into out there.