Among the many Zacks Rank #1 (Robust Purchase) listing a number of web commerce shares are standing out with earnings estimate revisions on the rise.

With the Web-Commerce Business presently within the high 11% of over 250 Zacks Industries here’s a take a look at a few of the top-rated shares within the house to contemplate shopping for amid the robust begin to 2023.

Alibaba BABA

Beginning the listing is Alibaba, which has been among the many Zacks Rank #1 Robust Buys since January 18 with its inventory climbing significantly throughout this time. Following the reopening of China’s economic system, Alibaba has been one of many pack leaders amongst Chinese language shares which have soared over the previous couple of months.

Alibaba’s fiscal 2023 earnings are actually anticipated at $7.20 per share which might be a -13% drop from a yr in the past however FY24 earnings are forecasted to rebound and climb 15% to $8.28 a share. Even higher, earnings estimate revisions have began to go up once more for FY23 with FY24 estimates up 5% during the last quarter.

Picture Supply: Zacks Funding Analysis

Earnings estimates persevering with to rise for Alibaba is an efficient signal as BABA inventory is up +52% within the final three months to simply outpace the S&P 500’s +11%. Plus, buying and selling round $106 a share Alibaba inventory nonetheless trades attractively relative to its previous at 18.5X ahead earnings. That is 72% beneath its historic excessive of 66.6X and a 50% low cost to the median of 36.9X one other indication that there might be extra upside from present ranges.

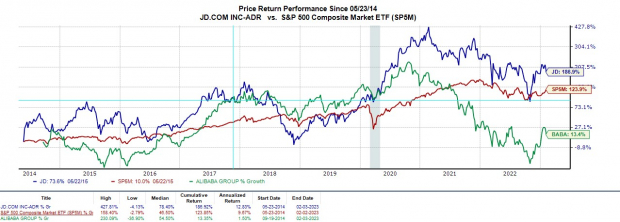

JD.com JD

JD.com is one other Chinese language internet-commerce inventory which will even have extra upside with its inventory skyrocketing prior to now few months as effectively. During the last three months, JD inventory is up +30% to beat the benchmark and has been on par with the Digital Commerce Markets +31% regardless of trailing Alibaba’s +52%.

Extra spectacular, since going public in 2014, JD inventory is now up +187% which has topped Alibaba’s +13% throughout this era and the S&P 500’s +124% and reveals the corporate could be very a lot a viable choice with regard to E-commerce development in China.

Picture Supply: Zacks Funding Analysis

With the big measurement of China’s inhabitants, there may be definitely sufficient room for each Alibaba and JD.com as elite gamers in regard to direct-to-consumer product gross sales by way of their on-line platforms. To that word, JD.com’s earnings estimates have gone up for its present fiscal 2022 and FY23.

Fiscal 2022 earnings are actually projected to climb 44% to $2.44 per share in comparison with EPS of $1.69 in FY21. Fiscal 2023 earnings are forecasted to rise one other 14%. Buying and selling at $57 a share and 27X ahead earnings JD inventory trades effectively beneath its absurd historic excessive of two,100.5X and at a 60% low cost to the median of 68.9X.

Match Group MTCH

Rounding out the listing is North American-based courting platform operator Match Group which was just lately added to the robust purchase listing together with JD.com.

With earnings estimates trending greater, Match inventory is beginning to stick out as MTCH remains to be 67% off its 52-week highs. Whereas there isn’t any assure Match will eclipse a really spectacular excessive of $118.95 per share final February, fiscal 2023 earnings are projected to climb a powerful 72% to $2.15 per share in comparison with EPS of $1.25 in FY22.

Picture Supply: Zacks Funding Analysis

Plus, FY24 earnings are projected to leap one other 14% with MTCH inventory buying and selling at $48 per share and 24.4X ahead earnings. That is 90% beneath its historic excessive of 249X and a 43% low cost to the median of 43.2X with Match inventory now up 15% during the last month to high the current rallies within the broader indexes.

Backside Line

With these Web-Commerce shares buying and selling attractively relative to their previous, the rising earnings estimate revisions are a fantastic signal that there might nonetheless be extra upside left after their current rallies. The annual backside line development can also be spectacular and creates long-term worth along with the near-term upside with their common Zacks Worth Targets effectively above present ranges.

Zacks Names “Single Greatest Choose to Double”

From hundreds of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have probably the most explosive upside of all.

It’s a little-known chemical firm that’s up 65% over final yr, but nonetheless grime low-cost. With unrelenting demand, hovering 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail buyers might leap in at any time.

This firm might rival or surpass different current Zacks’ Shares Set to Double like Boston Beer Firm which shot up +143.0% in little greater than 9 months and NVIDIA which boomed +175.9% in a single yr.

Free: See Our Top Stock and 4 Runners Up >>

JD.com, Inc. (JD) : Free Stock Analysis Report

Alibaba Group Holding Limited (BABA) : Free Stock Analysis Report

Match Group Inc. (MTCH) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the writer and don’t essentially mirror these of Nasdaq, Inc.