This is only one story of the thousands and thousands of Individuals whose lives have been modified by the Inexpensive Care Act. This sort of change has been a very long time within the making.

After almost 100 years of discuss, and many years of making an attempt, President Obama lastly made inexpensive, high quality well being take care of all a actuality for America. At present, 20 million extra adults have medical health insurance. Three million extra youngsters have medical health insurance than in 2008. America’s uninsured price now stands at its lowest stage ever. 100 and 5 million Individuals now not have lifetime limits on their protection and 137 million Individuals now have a proper to protection for important preventive companies with no out-of-pocket prices, like flu photographs, yearly check-ups for ladies, and contraception.

Irrespective of who you might be, likelihood is you are benefiting from an improved well being care system because of the Inexpensive Care Act. It’s possible you’ll not notice that there is a lot to lose if Republicans reach repealing this regulation. Here is a take a look at a couple of completely different situations that replicate the lives of many Individuals, and what occurs with and with out this regulation in place.

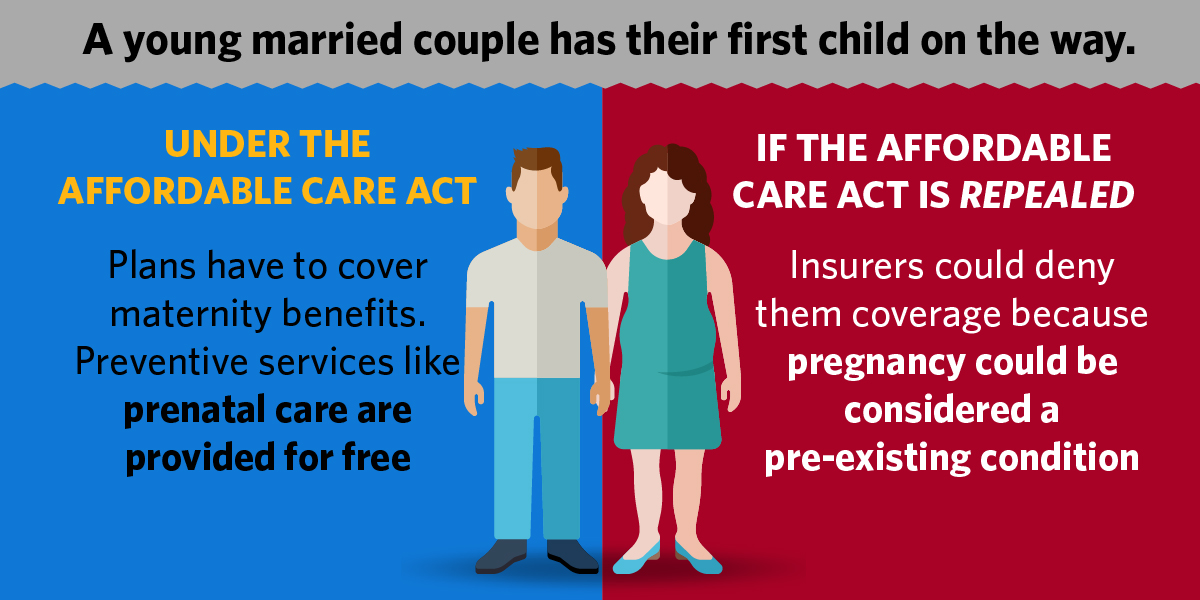

A younger married couple obtain information that they’re going to have their first youngster, and resolve to maneuver nearer to their household. Because of the Inexpensive Care Act (ACA) they will discover well being care protection by way of the Market despite the fact that their new jobs, which have a mixed earnings of $40,000, don’t present protection.

Extra on how the ACA helps:

- They’re able to simply go browsing and evaluate plans to seek out one which works for them. On account of their transfer, they qualify for a particular enrollment interval, and may select a plan that gives protection straight away.

- What’s extra, they obtain monetary help that gives over $4,250 a yr to scale back their premiums, overlaying over 55 p.c of the associated fee, in addition to reduces their out-of-pocket prices.

- Because of the patron protections within the ACA, their plan covers maternity advantages. It additionally covers preventive companies like prenatal care with no out-of-pocket prices.

- She goes to a hospital that takes half within the voluntary ACA program that helps to forestall pointless early deliveries and maximize the well being of the mother and child. The household can also qualify for a house go to that gives finest practices for brand spanking new mother and father.

- The newborn’s immunizations and effectively youngster go to are coated with no out-of-pocket price.

If the ACA had been repealed:

- Being pregnant might be thought of a pre-existing situation, which means when this household regarded for brand spanking new protection after transferring, insurers may deny them protection or cost exorbitant charges.

- Their plan would seemingly not embody maternity protection, as was the case for over 60 percent of enrollees in particular person market plans in 2011.

- They’d obtain no monetary help to assist guarantee they will discover a good plan inside their funds. They’d obtain no assist in paying their out-of-pocket prices.

- The applications that assist wholesome pregnancies, births, and newborns would now not exist, placing the household at better danger of well being issues.

- And the household would seemingly need to pay out of pocket for every go to and shot for his or her new child, placing them additional behind on different family funds.

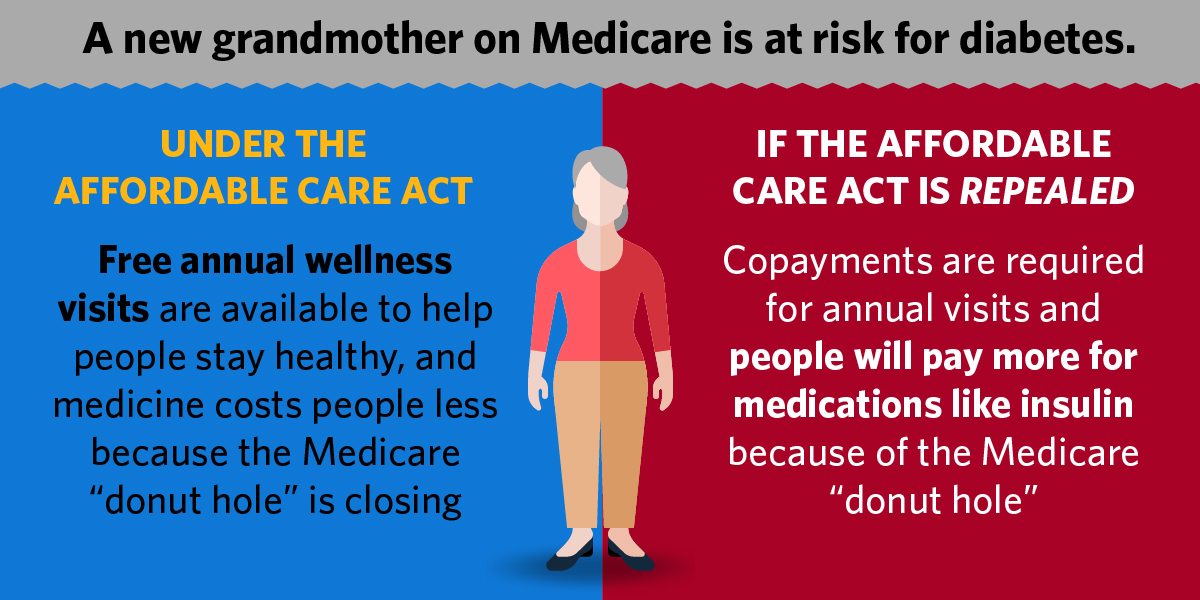

A Medicare beneficiary with pre-diabetes later develops diabetes, with vital related prices and problems. She additionally suffers a fall and a subsequent hospitalization. The preventive companies out there by way of the ACA assist her delay the onset of diabetes, and the ACA additionally helps to forestall additional hospitalization and cut back medical issues. This permits the brand new grandmother to spend extra time along with her granddaughter.

Extra on how the ACA helps:

- She will obtain a free annual wellness go to, together with a diabetes screening. Her physician diagnoses her with pre-diabetes, which means her blood sugar is excessive and he or she is in danger for growing diabetes sooner or later.

- Her doctor refers her to a Diabetes Prevention Program, which Medicare will begin paying for nationwide. This Program suggests enhancements in her weight loss plan and encourages her to extend her bodily exercise, serving to her drop extra pounds and lowering her probabilities of growing diabetes.

- When she suffers a severe fall and is hospitalized, her hospital has improved affected person security practices because of the ACA, lowering the prospect of her buying a probably lethal an infection throughout her keep.

- Moreover, her hospital has improved its coordination with dwelling well being and different post-acute care suppliers, offering her with a clean transition from the hospital again to her dwelling, serving to her recuperate extra shortly and stopping a pricey readmission to the hospital.

- Whereas preventive measures delay her growth of diabetes, after 5 years, she does develop diabetes and requires insulin, which she will get by way of her Medicare Half D prescription drug plan. On account of the ACA phasing out the Medicare “donut gap,” affected beneficiaries have saved a mean of $2,127 on pharmaceuticals by way of July 2016, and her financial savings on these medicines will enhance yearly till the “donut gap” is fully closed in 2020.

If the ACA had been repealed:

- She would pay a copayment for her annual go to to her doctor, which may trigger her to skip the go to so as to lower your expenses.

- In consequence, she wouldn’t study that she has pre-diabetes. Even when she had been lastly recognized with pre-diabetes, Medicare wouldn’t pay for the Diabetes Prevention Program, and thus she may shortly develop full-blown diabetes.

- Due to the reopening of the Medicare “donut gap,” she would pay considerably extra for her insulin and different medicines, consuming into her restricted earnings and probably inflicting her to skip doses so as to lower your expenses.

- When she is lastly discharged dwelling after her fall, she wouldn’t have any help to assist her perceive her medicines or the best way to contact the house well being company that may present her observe up care. The unmanaged transition could lead on her well being to shortly deteriorate, leading to a readmission to the hospital.

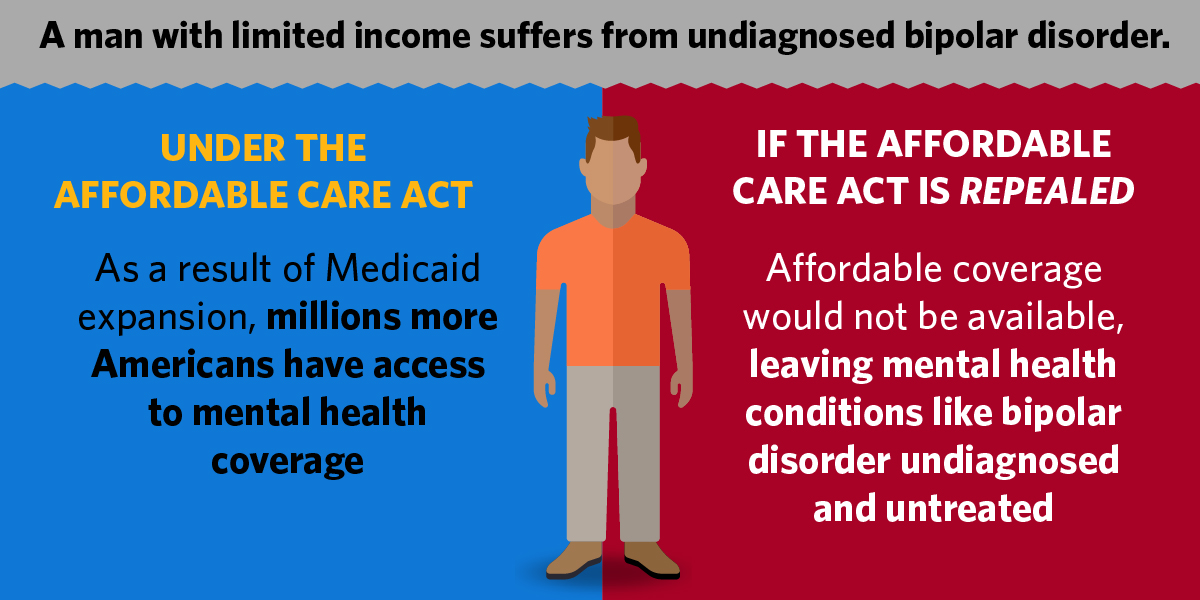

A person with a low earnings suffers from undiagnosed bipolar dysfunction. Because of the ACA, he has entry to non-public insurance coverage, regardless of his pre-existing situation, and to Medicaid in his state, and each have sturdy protections for enrollees with psychological well being challenges. As a result of his annual earnings is $12,000, he qualifies for Medicaid.

Extra on how the ACA helps:

- People with incomes as much as 133 p.c of the federal poverty stage are actually eligible for Medicaid enlargement in States that select to broaden.

- With protection beneath his State’s Medicaid enlargement, he is ready to get the care and remedy he wants.

- If his earnings rises by $5,000, he’ll qualify for personal particular person medical health insurance with monetary help. For the primary time, this man can’t be denied protection based mostly on a pre-existing psychological well being situation.

- Particular person market protection should embody psychological well being and substance use dysfunction companies as an “important well being profit” and the protection have to be usually akin to the advantages supplied for medical and surgical advantages.

If the ACA had been repealed:

- He wouldn’t afford protection or physician’s visits, and would haven’t any common supply of major care, so his situation would stay undiagnosed.

- On account of his lack of normal care, he would go to the emergency room incessantly to obtain care.

- Missing protection, he could be unable to afford remedy or to see a psychiatrist, which might trigger his situation to worsen. Such circumstances typically result in substance use issues.

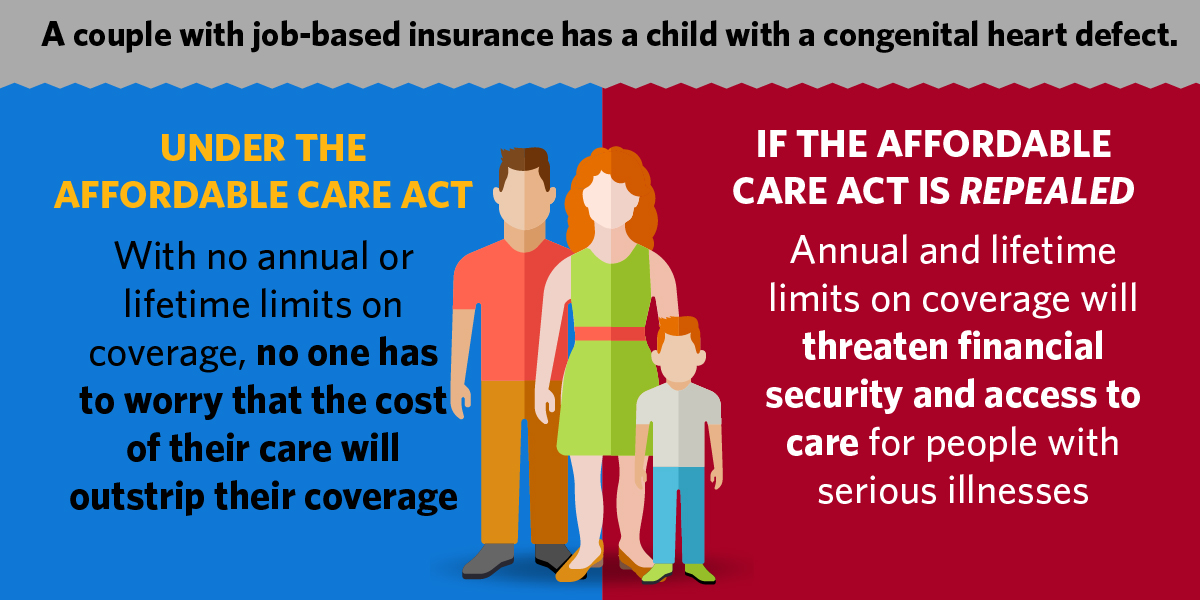

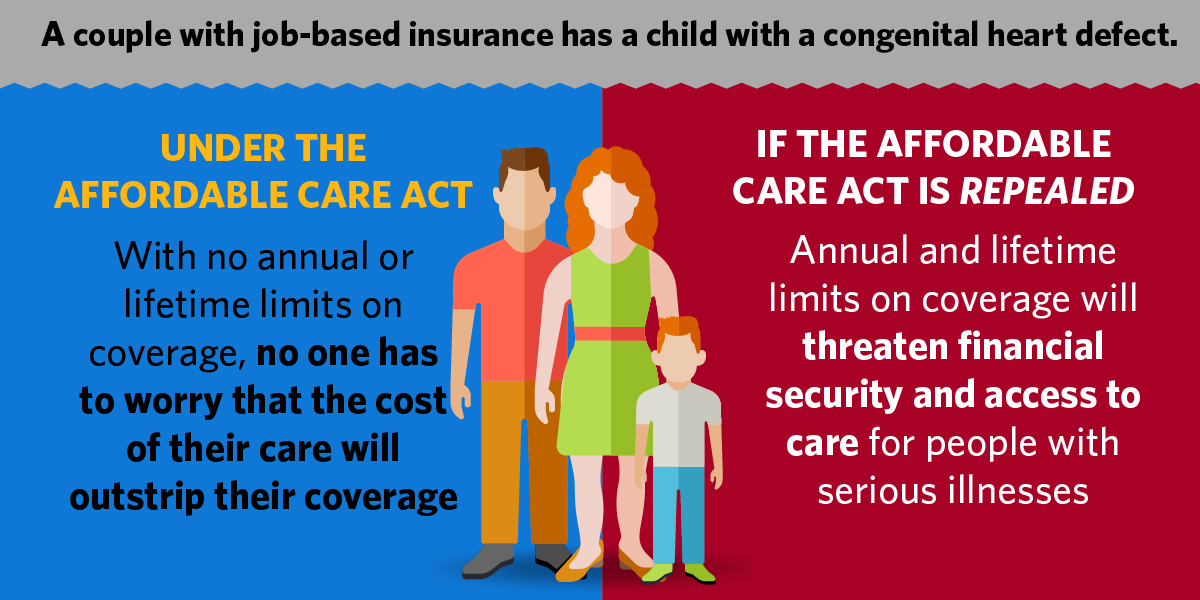

A pair with insurance coverage by way of their employer provides start to their second youngster, who’s born with a congenital coronary heart defect. Due to the complexity of the defect, the kid requires quick specialised care and can proceed to wish particular coronary heart care all through his life. The ACA helps this household by stopping them from reaching an annual or lifetime restrict on what insurance coverage will cowl. And, this youngster will at all times be insurable despite the fact that he has a pre-existing situation.

Extra on how the ACA helps:

- There isn’t any annual or lifetime greenback restrict on the couple’s insurance coverage plan. Because of this they won’t have to fret about medical chapter due to the excessive price of their son’s care. Previous to the ACA, 105 million individuals with employer plans had lifetime limits on their protection, encompassing 59 p.c of all staff coated by their employer’s well being plan.

- Their employer-provided plan additionally should now cap the out-of-pocket prices they will pay, and because the ACA turned regulation a further 22 million individuals have gained safety in opposition to catastrophic prices.

- As well as, the ACA permits them to maintain their son on their plan till he’s 26, so they don’t have to fret about how he’ll get hold of protection sooner or later, which was a major problem for a lot of younger adults. Previous to the ACA, one in three younger adults between the ages of 19 and 25 had been uninsured.

- And, due to the ACA’s ban on insurer discrimination in opposition to particular person’s with pre-existing situations, these mother and father would not have to fret about whether or not their son can entry protection when he’s now not on their plan.

If the ACA had been repealed:

- This couple would face vital monetary burdens in caring for his or her son. Given the numerous prices related to caring for advanced coronary heart defects, they might in a short time attain the lifetime restrict on their plan, along with the numerous out-of-pocket prices they might incur.

- They’d then be pressured to both discover a new job that supplied protection and not using a lifetime restrict or discover a technique to pay for the prices of their son’s care on their very own.

- As well as, their employer’s plan wouldn’t essentially have to cowl their son till age 26, which means that, as soon as he’s older, he would wish to seek out an alternate supply of protection to offer for his ongoing care.

- And, due to discrimination in opposition to people with pre-existing situations, he could not ever be capable of get hold of protection once more.

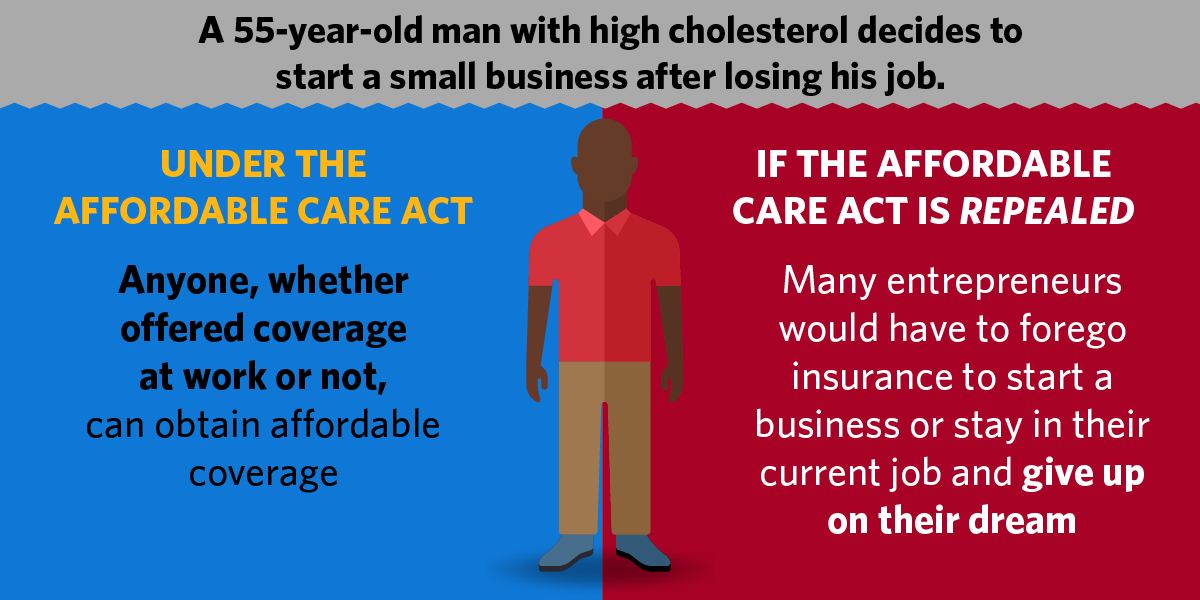

A 55-year-old man with a historical past of excessive ldl cholesterol loses his job. He decides to start out his personal small enterprise. The ACA helps him discover inexpensive well being protection despite the fact that he has a pre-existing situation. And, it makes it simpler for him to offer medical health insurance to his staff as his small enterprise grows by offering tax credit and guaranteeing premium {dollars} go to offering care somewhat than padding insurers’ earnings.

Extra on how the ACA helps:

- He is ready to get hold of protection on the Market after dropping his job, which means that he’s free to start out his personal enterprise somewhat than work for a big enterprise simply to maintain his well being protection.

- He can’t be discriminated in opposition to due to his excessive ldl cholesterol, which impacts over 73 million Americans.

- Furthermore, if his excessive ldl cholesterol results in a coronary heart assault or different vital well being occasion, his insurer can’t cancel his plan over a technicality relating to the shape he crammed out when signing up for protection, resembling forgetting to report that he had rooster pox as a baby.

- All particular person market plans now cowl pharmaceuticals, so he can get hold of remedy to assist tackle his excessive ldl cholesterol and stop future well being issues.

- As his enterprise expands, he can use the Market for small companies to simply evaluate and store for plans for his staff and supply them a spread of choices that work for his enterprise and for them.

- An ACA provision requires that plans spend no less than 80 p.c of premiums on overlaying the price of care or making high quality enhancements, to make sure he’s getting the perfect worth for his greenback. Because of this provision, almost $2.8 billion in rebates have been paid to Individuals from 2011-2015.

- And, due to the ACA, his small enterprise qualifies for a tax credit score value as much as 50 p.c of the associated fee he pays for his staff’ protection.

If the ACA had been repealed:

- This man would have vital bother discovering protection.

- To begin his personal enterprise, he would seemingly need to forgo insurance coverage, as his pre-existing situation would make it troublesome to seek out an inexpensive plan.

- He could be at risk of his insurer canceling his plan the second he had a major well being situation, and his plan won’t cowl the prescribed drugs he must deal with his excessive ldl cholesterol, as was the case for nearly one in ten individuals within the particular person market previous to the ACA.

- If he had been capable of begin his personal enterprise, he may discover it troublesome to offer well being take care of his staff, significantly given the dearth of a small enterprise tax credit score to assist offset prices.

- His staff, now pressured to seek out insurance coverage on their very own with out ACA eat protections, would face the identical kinds of points he did find protection. They might additionally favor to work for a corporation that gives well being advantages.

- And his insurance coverage firm may use much less of his premium {dollars} to offer care, as an alternative utilizing them to pay for advertising or firm earnings.

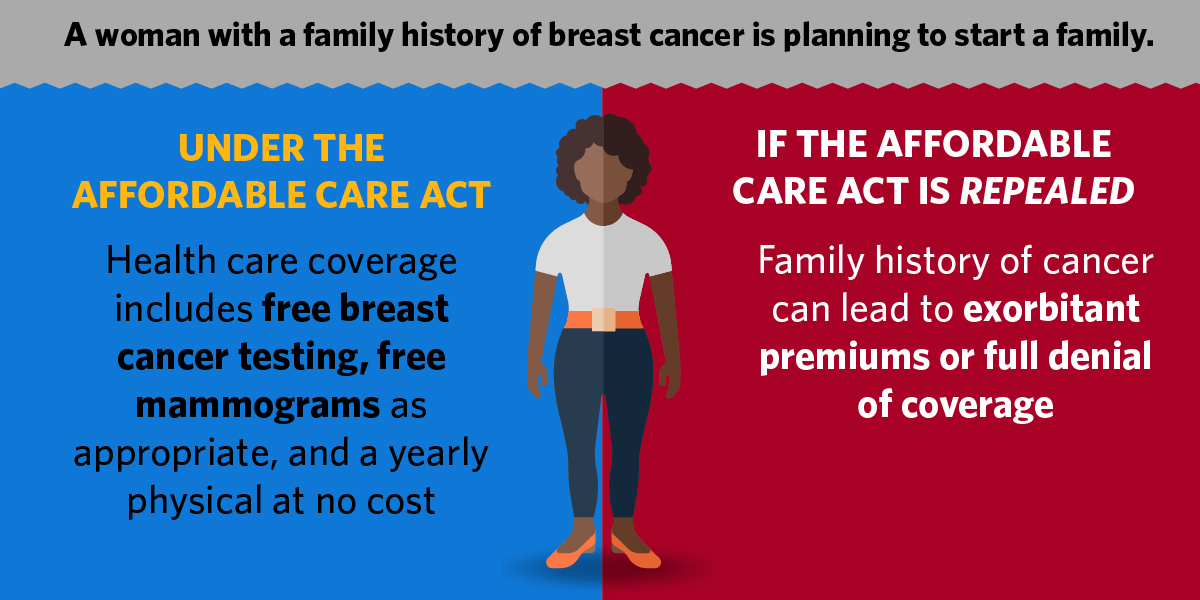

A newly married girl with a household historical past of breast most cancers is in search of a brand new particular person market insurance coverage plan. Because of the ACA, she will discover inexpensive protection regardless of her household historical past of break most cancers. Her protection will present free preventive companies to assist her handle her danger of breast most cancers. She can also be contemplating beginning a household. Her protection can even cowl vital preventive companies for ladies who could change into pregnant and supply her with contraception, each freed from cost.

Extra on how the ACA helps:

- She doesn’t want to fret that her household historical past of breast most cancers will probably be handled as a pre-existing situation that stops her from getting a suggestion of protection, being charged extra for protection, or having most cancers remedy excluded from protection.

- Her protection will embody free breast most cancers genetic take a look at counseling and, as she will get older, free mammograms as acceptable.

- And any protection that she receives will present a spread of free preventive screenings which can be vital for ladies who could change into pregnant.

- It’s going to additionally cowl a yearly bodily for gratis.

- As well as, she is going to be capable of get hold of contraception freed from cost, and her plan will probably be required to cowl care supplied at neighborhood well being facilities and household planning clinics.

If the ACA had been repealed:

- This girl may face vital issues discovering protection and making household planning selections which can be proper for her.

- She might be excluded from protection or charged exorbitant charges due to her household historical past.

- If she had been capable of finding protection, it might seemingly not present preventive companies freed from cost, making it tougher to handle her danger of breast most cancers.

- She would discover it tougher to interact in efficient household planning. Screenings might be pricey, and he or she must pay for contraceptive protection as effectively.

- She wouldn’t be assured an annual effectively girl’s go to with out out of pocket prices.

- And there could be no assure that her plan would cowl care at close by neighborhood well being facilities or household planning clinics, which may require her to journey vital distances to get wanted care at an inexpensive price.

Jeanne Lambrew is Deputy Assistant to the President for Well being Coverage.