Word: The next is an excerpt from this week’s Earnings Trends report. You’ll be able to entry the complete report that incorporates detailed historic precise and estimates for the present and following intervals, please click here>>>

Listed below are the important thing factors:

- The pattern of destructive estimate revisions that had reemerged over the previous few quarters — after reversing course earlier within the pandemic — has additional accelerated forward of the beginning of the 2022 This fall earnings season, with estimates for the present and coming intervals considerably coming down.

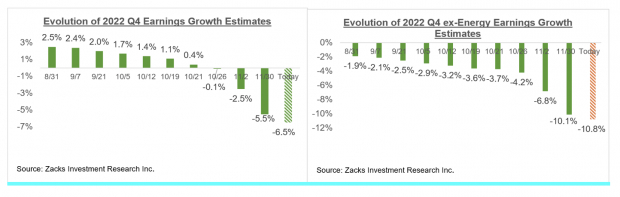

- For 2022 This fall, combination S&P 500 earnings are actually anticipated to be down -6.5% on +4.2% larger revenues. The -6.5% decline in index earnings right this moment is down from +1.7% on October fifth.

- Excluding the Vitality sector’s robust contribution from the S&P 500 index, This fall earnings for the remainder of the index are anticipated to be down -10.8% on +3.2% larger revenues. The -10.8% decline in index earnings right this moment is down from -2.9% on October fifth.

- This fall earnings estimates have come down for 13 of the 16 Zacks sectors for the reason that quarter acquired underway, with Transportation and Autos having fun with modest optimistic revisions and Aerospace estimates basically flat.

- By way of the magnitude of estimate cuts, the Primary Supplies and Client Discretionary sectors have suffered essentially the most, adopted by Development, Expertise and the Retail sectors. Even Vitality sector estimates have come down for the reason that quarter acquired underway.

- Full-year 2023 earnings estimates have been coming down after peaking in mid-April, with the mixture complete down -9.2% from the height for the index as an entire and -11.9% excluding the Vitality sector’s contribution.

- For the reason that mid-April peak, combination 2023 earnings estimates have declined for 13 of the 16 Zacks sectors, with the largest declines within the Development (down -27.1% in absolute phrases), Client Discretionary (-20.7%), Retail (-20.4%), Expertise (-19.4%), Primary Supplies (-15.4%), Industrial Merchandise (-13.9%), Aerospace (-13.4%) and Transportation (-9.3%).

- We strongly dispute the notion that earnings estimates stay out of sync with the financial floor actuality, notably if the financial slowdown ensuing from the Fed’s extraordinary tightening seems to be average.

- Wanting on the calendar-year image, complete S&P 500 earnings are anticipated to be up +4.6% in 2022 and +2.5% in 2023. On an ex-Vitality foundation, complete 2022 index earnings could be down -2.2% (as an alternative of +4.6%, with Vitality).

- The implied ‘EPS’ for the S&P 500 index, calculated utilizing the present 2022 P/E of 18.4X; and index shut as of December 14th is $217.36, up from $207.74 in 2021.

- Utilizing the identical methodology, the index ‘EPS’ works out to $223.73 for 2023 (P/E of 17.9X) and $241.20 in 2024 (P/E of 16.6X). The multiples have been calculated utilizing the index’s complete market cap and combination bottom-up earnings for every year.

The general image that emerged out of Q3 earnings season was one among stability and resilience, even because the destructive revisions pattern accelerated.

Earnings weren’t nice, however they weren’t unhealthy both. Many available in the market feared an earnings cliff that will pressure administration groups throughout many industries to offer downbeat steerage.

Not a lot development was anticipated given the place we’re within the financial cycle. However the precise development coming via the outcomes was ever so barely higher than anticipated. It’s this efficiency relative to expectations moderately than absolutely the stage of earnings or the expansion tempo that’s of relevance to the market.

Expectations for 2022 This fall and past have been reset decrease, as now we have been declaring for some time now. Analysts have been steadily slicing their estimates, reversing the optimistic revisions pattern that we witnessed in the course of the Covid quarters.

We noticed this within the run as much as the beginning of the Q3 earnings season, and the pattern continues with respect to estimates for the present interval (2022 This fall) and full-year 2023.

The charts under present how earnings development expectations for the 2022 This fall, as an entire and on an ex-Vitality foundation, have for the reason that quarter acquired underway:

Picture Supply: Zacks Funding Analysis

The chart under exhibits how the anticipated combination complete earnings for full-year 2023 have advanced on an ex-Vitality foundation:

Picture Supply: Zacks Funding Analysis

As now we have constantly been declaring, combination S&P 500 earnings exterior of the Vitality sector peaked in mid-April and have been steadily trending down ever since.

The Total Earnings Image

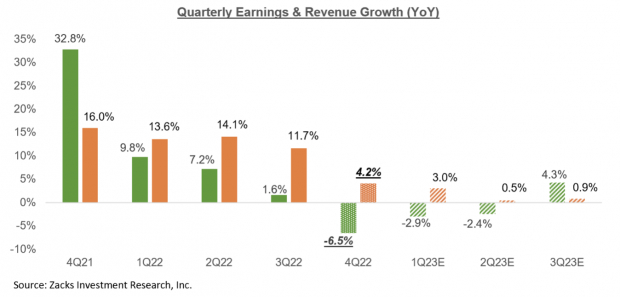

The chart under that gives a big-picture view of earnings on a quarterly foundation. The expansion charge for This fall is on a blended foundation, the place the precise experiences which have come out are mixed with estimates for the still-to-come firms.

Picture Supply: Zacks Funding Analysis

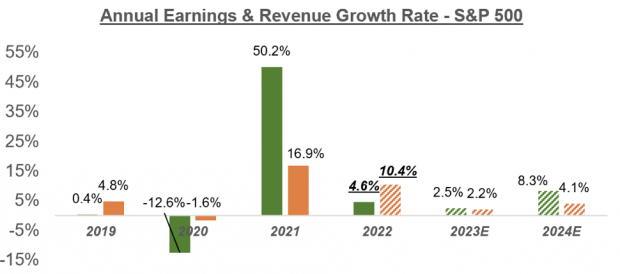

The chart under exhibits the general earnings image on an annual foundation, with the expansion momentum anticipated to proceed:

Picture Supply: Zacks Funding Analysis

As you possibly can see, earnings subsequent yr are anticipated to be up solely +2.5%. This magnitude of development can hardly be known as out-of-sync with a flat and even modestly down financial development outlook. Don’t overlook that headline GDP development numbers are in actual or inflation-adjusted phrases whereas S&P 500 earnings mentioned right here aren’t.

As talked about earlier, 2023 combination earnings estimates on an ex-Vitality foundation are already down by greater than -11% since mid-April. Maybe we see a bit extra downward changes to estimates over the approaching weeks, after the This fall reporting cycle actually will get underway. However now we have nonetheless already lined some floor in taking estimates to a good, applicable stage.

That is notably so if no matter financial downturn lies forward proves to be extra of the “backyard selection” than the final two such occasions. Recency bias forces us to make use of the final two financial downturns, which had been additionally among the many nastiest in current historical past, as our reference factors. However we must be cautious towards that pure tendency because the financial system’s foundations at current stay unusually robust.

7 Greatest Shares for the Subsequent 30 Days

Simply launched: Specialists distill 7 elite shares from the present checklist of 220 Zacks Rank #1 Robust Buys. They deem these tickers “Most Possible for Early Worth Pops.”

Since 1988, the complete checklist has crushed the market greater than 2X over with a median achieve of +24.8% per yr. So make sure you give these hand-picked 7 your instant consideration.

Invesco QQQ (QQQ): ETF Research Reports

SPDR S&P 500 ETF (SPY): ETF Research Reports

iPath Pure Beta Crude Oil ETN (OIL): ETF Research Reports

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.