This week’s selloff was intensified by financial considerations stemming within the monetary sector after the collapse of SVB Monetary Group’s (SIVB) Silicon Valley Financial institution.

Nevertheless, the broader selloff in markets is creating alternatives and listed below are three shares that traders ought to control.

Salesforce (CRM)

We’ll begin the checklist with a Zacks Rank #1 (Robust Purchase) as Salesforce’s inventory could be very intriguing in the intervening time. After crushing its This autumn high and backside line expectations final week Salesforce inventory had been seeing some good momentum.

The wrench that was thrown on the rally from broader financial considerations could provide traders a greater shopping for alternative. Moreover, a small correction might be wholesome and provide longer-term help.

Plus, earnings estimate revisions have been trending larger following Salesforce’s stellar fourth-quarter outcomes. This could proceed to be a catalyst for Salesforce inventory after the smoke clears from this week’s market decline.

Picture Supply: Zacks Funding Analysis

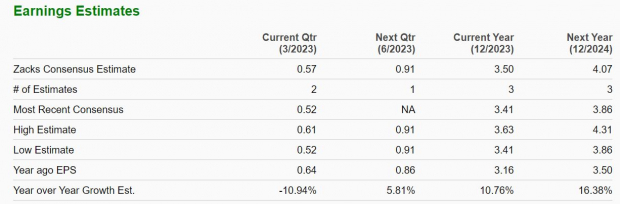

All through the quarter, Salesforce’s fiscal 2023 and FY24 earnings estimates have now soared 23% and 29% respectively. Fiscal 2023 earnings at the moment are anticipated to climb 33% and bounce one other 26% in FY24 at $8.75 per share.

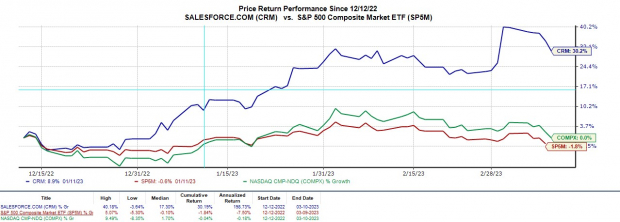

Even higher, Salesforce inventory continues to be up +31% 12 months up to now to largely outperform the S&P 500’s +2% and the Nasdaq’s +6%.

Picture Supply: Zacks Funding Analysis

Sterling Infrastructure (STRL)

Subsequent is Sterling Infrastructure which sports activities a Zacks Rank #2 (Purchase) and likewise gained some good momentum after the corporate lately introduced it was awarded a website growth mission for Hyundai’s EV battery facility.

That is on high of stellar progress in 2022 with earnings estimate revisions persevering with to pattern larger for fiscal 2023. Sterling’s earnings at the moment are anticipated to leap 11% in FY23 and climb one other 16% in FY24 at $4.07 per share.

Picture Supply: Zacks Funding Analysis

Sterling inventory continues to be up +18% 12 months up to now to largely outperform the broader indexes and its engaging valuation and stellar efficiency over the previous few years point out there may very well be extra upside forward.

Shares of STRL commerce at $38 and simply 11.6X ahead earnings which is properly beneath the business common of 19.9X and the S&P 500’s 17.9X. Plus, Sterling inventory trades far more fairly than its decade excessive of 298.8X and at a slight low cost to the median of 12.6X.

Picture Supply: Zacks Funding Analysis

EPR Properties (EPR)

Rounding out the checklist is EPR Properties which additionally sports activities a Zacks Rank #2 (Purchase). Many REITs have gotten engaging after the huge selloff among the many broader monetary sector and EPR’s inventory could also be price contemplating for its engaging valuation, numerous portfolio, and profitable month-to-month dividend.

EPR’s properties embody megaplex theatres, leisure retail facilities, lodging properties, and early childhood training facilities amongst others.

Buying and selling 33% from its 52-week highs EPR’s valuation is beginning to stand out. EPR trades at $37 per share and 8X ahead earnings which is properly beneath the business common of 12.5X and the benchmark.

Picture Supply: Zacks Funding Analysis

EPR additionally trades 68% beneath its decade excessive of 25.2X and at a 40% low cost to the median of 13.2X. Along with this, EPR’s 8.44% dividend yield blows away the REIT and Actuality Belief – Retail Markets 4.22% and the S&P 500’s 1.62%.

This could actually help affected person traders and revenue seekers as shares of EPR are down -9% YTD however are very engaging at their present ranges.

Picture Supply: Zacks Funding Analysis

Backside Line

Salesforce, Sterling Infrastructure, and EPR Properties shares seem like sturdy buy-the-dip candidates following this week’s selloff. There may very well be loads of upside forward for these shares as volatility subsides and we get again to what hopefully continues to be a rebound 12 months for a lot of equities.

Zacks Names “Single Finest Choose to Double”

From 1000’s of shares, 5 Zacks specialists every have chosen their favourite to skyrocket +100% or extra in months to return. From these 5, Director of Analysis Sheraz Mian hand-picks one to have essentially the most explosive upside of all.

It’s a little-known chemical firm that’s up 65% over final 12 months, but nonetheless filth low-cost. With unrelenting demand, hovering 2022 earnings estimates, and $1.5 billion for repurchasing shares, retail traders may bounce in at any time.

This firm may rival or surpass different current Zacks’ Shares Set to Double like Boston Beer Firm which shot up +143.0% in little greater than 9 months and NVIDIA which boomed +175.9% in a single 12 months.

Free: See Our Top Stock and 4 Runners Up >>

Salesforce Inc. (CRM) : Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL) : Free Stock Analysis Report

EPR Properties (EPR) : Free Stock Analysis Report

SVB Financial Group (SIVB) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.