Self-driving vehicles are one of many hottest subjects within the auto business, nonetheless, many view the adoption as “zero-to-one.” Mobileye (NASDAQ: MBLY), a longtime autonomous automobile chief, proves that the march towards full autonomy is incremental.

Mobileye creates superior driver-assistance techniques (ADAS) and provides them to automakers like Ford, GM, BMW, and Volkswagen. These techniques, which include cameras, sensors, and software program, allow “pc imaginative and prescient” to assist hold drivers protected on the highway.

Mobileye’s ADAS is answerable for a lot of these lane-assistance and computerized emergency braking options constructed into newer vehicles, and a few 42% of latest vehicles offered in 2022 had Mobileye know-how built-in.

Automakers are desirous to pay for these chips as a result of they obtain increased security scores whereas offering extra options to the top purchaser. Mobileye presently finds itself within the midst of a large spending ramp on ADAS know-how throughout the auto business, and because the market chief on this vertical, the corporate stands to vastly profit.

With robust top-line progress already, Mobileye may see its success skyrocket as key developments within the auto business proceed to unfold.

Earnings within the auto business imply promoting vehicles which can be about greater than getting from level A to level B. Automakers perceive that discretionary options are high-margin gadgets, so even base-model vehicles now include bells and whistles. With the arrival of latest driver help know-how, automakers can now supply extra superior options that improve the security of their autos and command increased costs.

This pattern is already in movement, with most automakers opting to supply higher-priced autos and pack them with extra superior options—margin over quantity. The common value of a brand new automotive within the US is now over $49,000, according to Kelley Blue Book. And superior driver-assistance techniques (ADAS) are one-way automakers differentiate themselves and meet shopper demand. Heated seats and navigation don’t lower it at as we speak’s new automotive costs.

And the auto business is amid a large ramp in spending on ADAS know-how, with penetration charges already set to surpass 80% in US automobile gross sales in 2023 for stage 0 ADAS. Nonetheless, lower-level ADAS are decrease margin models for Mobileye. Whereas supplying the business with entry-level ADAS led to critical top-line progress and a whopping 69% market share within the vertical, we’re nonetheless in very early innings concerning the true progress.

It’s the extra subtle options which can be but to penetrate the mass automobile market and as of now, are relegated to the luxurious automakers. As an illustration, in line with Counterpoint’s US Autonomous Vehicle Tracker, lower than 4% of latest vehicles within the US ship with stage 2+ ADAS options.

![]()

As stage 0 and stage 1 ADAS develop into the usual for brand spanking new vehicles, automakers will start to splurge for the extra superior, higher-margin techniques. And Mobileye is effectively positioned to profit from the continued adoption of stage 2+ autonomous options in vehicles, as the corporate already has a $17 billion backlog by way of 2030, including significant revenue from their most superior merchandise like Mobileye SuperVision, which is an “eyes-on, hands-off” system already being carried out in Chinese language EVs. These extra superior merchandise have a lot increased common gross sales costs per unit than their normal ADAS options.

Then there’s the catalyst of electrical automobile adoption. Carrying a a lot increased common gross sales value than conventional autos, EVs are additionally full of far more than ADAS know-how. As soon as a luxurious area of interest, EVs are going mainstream and are slated to develop at a 22.5% CAGR by way of 2030, offering further gasoline to Mobileye’s progress story.

Mobileye’s inventory has been on fireplace recently, returning 23% year-to-date, thanks partly to Wall Avenue’s renewed curiosity in AI and automation shares. Leaders of the rally, like C3.ai (NYSE: AI) are posting year-to-date returns north of 100%.

Nonetheless, traders ought to look to 3 key catalysts to evaluate whether or not Mobileye inventory will profit from current enthusiasm across the inventory.

Watch The Float

Mobileye broke from custom in promoting solely about 5% of its excellent shares in its October 2022 IPO, in comparison with the same old 10-20% that usually transfer in an IPO. This implies there’s a good provide of Mobileye shares, and the inventory value may expertise a disproportionate impact within the face of a surge in demand.

Moreover, the corporate has an unusually excessive quick curiosity, representing roughly 14% of the float.

Convention Participation

As a younger inventory, Wall Avenue hasn’t gotten to know Mobileye but, with corporations solely initiating protection on the inventory in current months. Which means there’s quite a lot of thriller surrounding the corporate.

The corporate’s participation in two investor conferences this week may present key perception into the upcoming quarter and different catalysts. It’s frequent for shares to rise resulting from an investor convention, particularly recent IPOs. With Mobileye being one of many solely profitable tech IPOs in current reminiscence, Wall Avenue may have its ear to the bottom.

Mobileye will be participating in each the Citi 2023 World Industrial Tech and Mobility Convention on Wednesday, February 22, and the Barclays Industrial Choose Convention on Thursday, February 24.

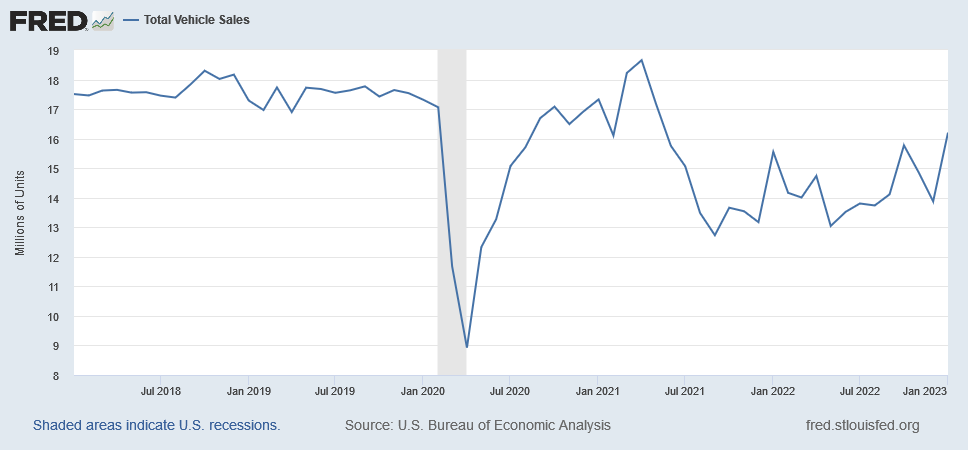

Watch Automobile Gross sales

Automobile gross sales stay unusually robust regardless of an inflationary regime the place many customers are gearing up for a recession. Mobileye’s enterprise closely depends on new automotive gross sales remaining. Under is a chart of latest automobile gross sales during the last 5 years:

Whereas Wall Avenue is sort to Mobileye now, worries about automotive gross sales and the corporate’s excessive valuation will mount if it doesn’t proceed its progress trajectory and justify its excessive valuation given its lack of profitability.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially mirror these of Nasdaq, Inc.