By John Hyland

Since its starting nearly 30 years in the past the ETF business sees a brand new pattern or product emerge each few years. From sector funds to commodity funds to mounted revenue funds to lively funds to thematic funds and to non-fully clear portfolios, one thing new comes alongside like clockwork. Every innovation raises the query of if the most recent factor will achieve traction? Will it grow to be enormous? Or will it fizzle out? 2021 was no exception. We noticed for the primary time the conversion of a mutual fund into an ETF.

Though it has been lower than two years since this latest function on the ETF panorama, there may be motive to imagine this could be a significant shift. Since March of 2021, 33 mutual funds, with nearly $60 billion in AUM, transformed themselves into ETFs. Towards the background of an nearly $7 trillion-dollar US-based ETF universe, $60 billion could appear pretty small. Nonetheless, a lot of this cash got here from fund companies that weren’t beforehand ETF issuers. This new inflow in nicely beneath two full years is definitely spectacular.

The benefits of an ETF over a mutual fund for the investor are in fact pretty well-known. ETFs are usually extra tax environment friendly, supply higher transparency, and are sometimes, though not at all times, a bit cheaper than the choice mutual fund. Particularly if the funds are actively managed.

Nonetheless, simply because an ETF provides sure benefits to the investor doesn’t utterly clarify why the mutual fund CEO would undertake the conversion. They want their very own compelling enterprise motive to take action. Notably if they’re going to be reducing charges. What might that motive be? There’s a good likelihood the reason being truly worry.

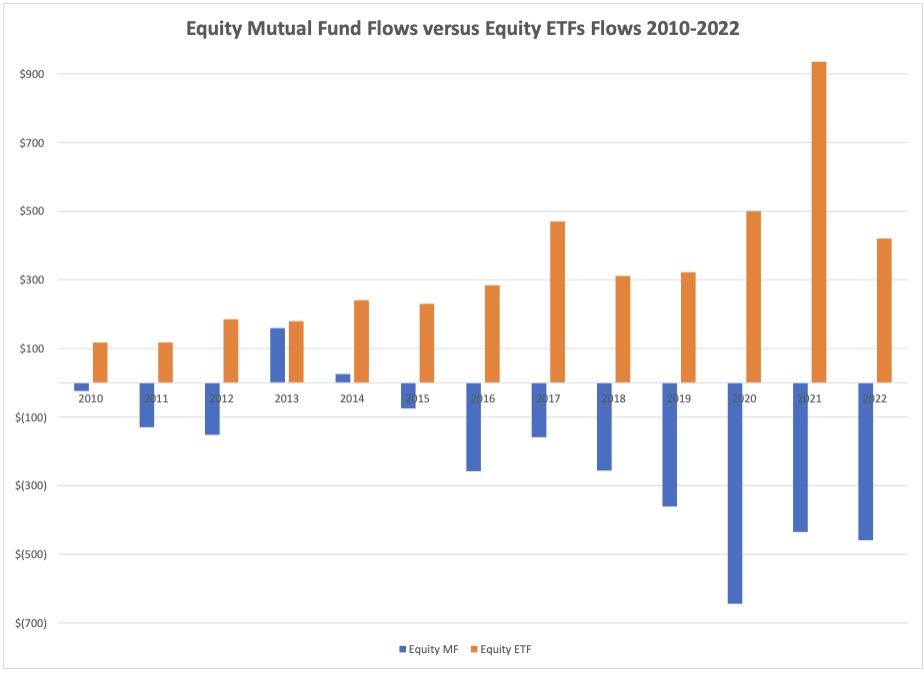

Because the World Monetary Disaster of 2008-2009, flows of latest cash into mutual funds have positively taken a flip for the more serious. Particularly in comparison with new cash flows into ETFs. The primary chart beneath compares annual flows of latest cash into fairness mutual funds versus fairness ETFs from 2010 to 2022. Clearly flows of cash into fairness mutual funds, each lively and passive, have been unfavourable for many of the final 12 years and the pattern is getting worse. In the meantime flows into fairness ETFs have been constructive yearly and have been trending up.

In case you are the CEO of a purely mutual fund firm, and also you take a look at this chart and the pattern, it ought to definitely ship shivers down your backbone. Certain, your gross sales and distribution staff could also be elevating $10 billion in a yr in new gross sales, however you probably have $20 billion in redemptions, and also you see the hole is rising yr by yr, it’s too straightforward to think about the place you’ll be in 10 extra years.

For some time the flows in bond mutual funds regarded much less grim. The chart beneath is flows into mounted revenue mutual funds and ETFs over the identical 2010-2022 interval. Three issues bounce out from the information. First, the tendencies don’t seem as dangerous as for fairness mutual funds as bond mutual funds appeared to have achieved nice for many of this time interval helped little doubt by a seek for yield in a low rate of interest setting. Nonetheless, two tendencies counsel that mutual fund CEOs needs to be much less sanguine even right here. First, it’s obvious that bond ETF flows are quickly catching up with bond mutual fund flows in good years. In 2010 flows into bond ETFs had been solely 13% of the flows in bond mutual funds. Lately flows into bond ETFs have common extra like 50%-80%. Not pattern for mutual funds, nevertheless it will get worse. In years the place bond mutual funds have unfavourable flows bond ETFs nonetheless have constructive new money circulation. This has been significantly true in 2022, a yr the place bond funds of each wrappers have seen unfavourable returns. But bond ETFs nonetheless are seeing new flows whereas bond mutual funds are seeing main outflows.

One potential rationalization for the bond circulation tendencies, in addition to the fairness flows, is that when many traders promote mutual funds, both to reinvest in a distinct technique or just to interact in tax loss harvesting, they in the end put the cash again into the market. Nonetheless, these tendencies would possibly counsel they purchase their new holding as an ETF and never as a mutual fund. If true than when you repeat this sample over the course of a number of bull and bear markets the impression on mutual fund flows could be huge.

To deal with this situation, we requested a longtime ETF gross sales and distribution veteran how a lot of an element he thought this form of switching between wrappers was at current. His response was there may be loads of anecdotal proof to counsel that the tax loss harvesting transfer from mutual fund to ETF is a really actual pattern.

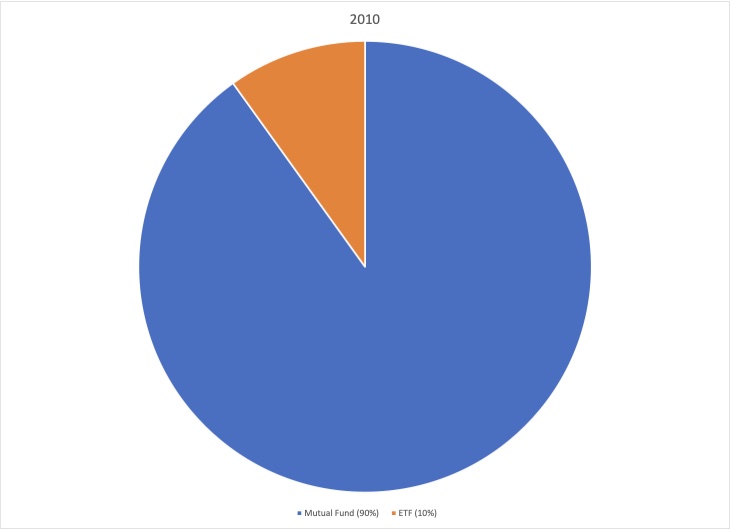

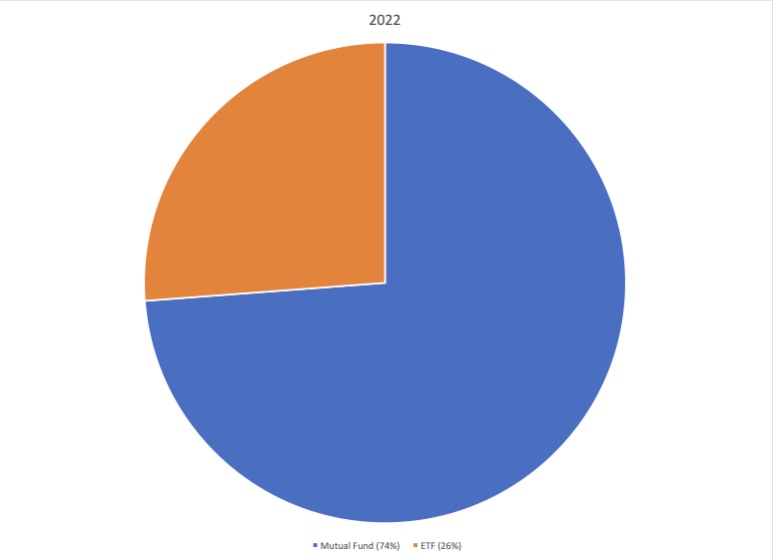

The place will this take us within the close to future? In the event you take a look at the 2 pie charts beneath you’ll be able to see that in contrast that the share of the asset pie held by ETFs has risen an amazing deal since 2010 in comparison with mutual funds. The charts are all belongings held by each mutual funds and ETFs (excluding cash market funds). ETFs share of the entire has risen from 10% to 26%. In absolute {dollars} each slices rose an amazing deal pushed by the lengthy bull market of the final decade, however ETFs had been helped by new funding flows whereas the mutual fund slice was negatively impacted.

After all, the pattern proven above was achieved with primarily no contribution from the conversions. If conversions grow to be a significant component the ETF slice might primarily simply eat up the mutual fund slice.

these tendencies this raises an excellent query. Why, as a matter of enterprise technique, don’t mutual fund CEOs simply plan to transform extra, or most, of their mutual funds into the wrapper that appears to be getting all of the flows? Is it simply stubbornness or are there sensible causes to carry off on pulling the set off on main conversions?

To deal with this situation, we requested Vettafi’s well-known ETF guru Dave Nadig what may be stopping a mutual fund exec staring down into the abyss why they’d NOT make a swap?

“In the event you’re sitting on a passel of well-known lively mutual funds, you have got an actual conundrum. In the event you convert every little thing into ETFs, likelihood is it’s a must to try this on the lowest out there value for every technique. Nonetheless promoting some 1% A-Shares with a load? Sorry, that’s not going to fly, you’re going to finish up utilizing that 60bps “cleanshare” because the benchmark in your ETF pricing, otherwise you’re not going to achieve belongings. So that may imply a direct brief time period hit to income. That may be a tough tablet to swallow.

It will get worse although. Chances are high numerous your belongings come from outlined contribution plans. You principally can’t convert these shares in any respect, as a result of most mutual funds in DC plans pay a 12b1 payment to offset recordkeeping (almost exceptional in ETFs). Additionally, these recordkeepers are possible not interested by your whole-ETF shares, they’re designed to trace the simply fractionated mutual fund shares.

These two dynamics – pricing and fractional shares – are why you’ve seen lots of the true conversions in tax-aware methods (e.g. DFAs conversions), and why others, like Constancy, have been pressured to create clones of fashionable methods reasonably than convert (e.g. FMAG).”

Clearly there are causes for a CEO to not transfer all of their mutual funds into ETFs. Or not less than causes to not achieve this straight away. In response to the Funding Firm Institute knowledge 17% of mutual fund belongings are in 401(okay) plans. The opposite 83% is presumably held in accounts that would extra simply simply use an ETF in substitute of a mutual fund. However 17% is a mean. For some mutual fund households their proportion of AUM in 401(okay)s may be nicely beneath 10%, making the choice to transform a lot simpler. Others will probably be over 25%, making the choice a lot harder.

Lastly, this raises the query of if many mutual funds solely companies, or companies whose mutual fund enterprise dwarfs their ETF enterprise, are at the moment doing conversions. Companies like Constancy have all already introduced or filed to do such conversions. Is that this simply the tip of the iceberg? We return to our veteran ETF capital markets director. “In the event you discuss to the oldsters on the inventory exchanges and on the custodian banks, they are going to let you know the phone is ringing off the hook with calls from mutual fund companies. Calls are coming in sooner than they’ll reply.”

For extra information, info, and evaluation, go to the ETF Education Channel.

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.