Word: The next is an excerpt from this week’s Earnings Trends report. You may entry the complete report that comprises detailed historic precise and estimates for the present and following intervals, please click here>>>

Listed below are the important thing factors:

- The image rising from the 2022 Q3 earnings season belies pre-season fears of an impending earnings cliff. The general company profitability image isn’t nice, nevertheless it isn’t dangerous both.

- For the 62 S&P 500 members which have reported Q3 outcomes already, complete earnings are down -4.6% from the identical interval final 12 months on +8.8% greater revenues, with 77.4% beating EPS estimates and 59.7% beating income estimates.

- With respect to constructive surprises, the proportion of those 62 index members beating EPS estimates is under the 5-year common, however in any other case inside the historic vary, although the income beats proportion is on the decrease facet.

- 2022 Q3 as a complete, complete S&P 500 earnings are at the moment anticipated to be up +0.6% from the identical interval final 12 months on +9.1% greater revenues. Excluding contributions from the Power sector, Q3 earnings for the remainder of the index can be -6.0% under the year-earlier degree.

The continuing Q3 earnings season seems to be a replay of what we witnessed within the June-quarter reporting cycle, when estimates and sentiment had weakened a lot that the precise outcomes find yourself trying loads higher as compared.

Having seen outcomes from about 12% of S&P 500 members by now, we will see that outcomes are not at all nice, however they aren’t dangerous both. It’s all about expectations and people had been adjusted decrease forward of the beginning of this earnings season. Importantly, many available in the market appeared prepared for earnings to ‘fall off the cliff’, with administration groups guiding decrease. Now we have seen a few of that, however for essentially the most half the long-feared growth has not materialized, no less than not but.

You will need to level out that the pattern of outcomes at this stage is weighted in the direction of the Finance sector, whose profitability advantages from greater rates of interest. Financial institution of America BAC actually stood out on that rely, however virtually all the banks got here out with robust numbers for Q3 and offered reassuring commentary for This autumn. There have been good numbers outdoors of Finance as effectively, with the early outcomes from air carriers like United Airways UAL, truckers like J.B. Hunt JBHT, beverage and meals gamers like Pepsi PEP and Basic Mills GIS all exhibiting energy.

We should always remember that these operators within the consumer-facing beverage, meals and different product classes have been in a position to move on the upper price of inputs, labor, and logistics so far. However we will intuitively admire that the development can’t go on ceaselessly.

We noticed a few of that within the Proctor & Gamble PG report whose natural gross sales have been up in Q3 on the again of worth will increase, however administration indicated that they might have reached the restrict in how a lot they may increase costs going ahead.

The associated fee headwinds have been with us for some time, as has been the difficulty of foreign-exchange translation points. However the U.S. greenback’s file energy this 12 months has develop into a a lot greater hurdle for firms. In reality, P&G was pressured to trim its steering solely on FX grounds.

All of this collectively is weighing on estimates for the present and coming intervals, as we’ve been mentioning on this area. We noticed this within the run as much as the beginning of the Q3 earnings season and the development continues with respect to estimates for the present interval (2022 This autumn) and full-year 2023.

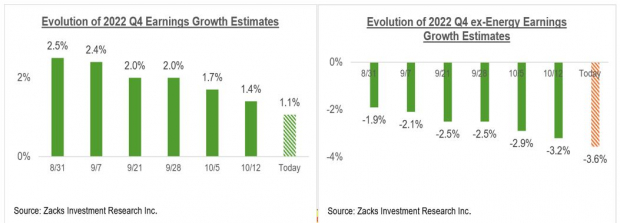

The charts under present how earnings progress expectations for the 2022 This autumn, as a complete and on an ex-Power foundation, have developed in current weeks.

Picture Supply: Zacks Funding Analysis

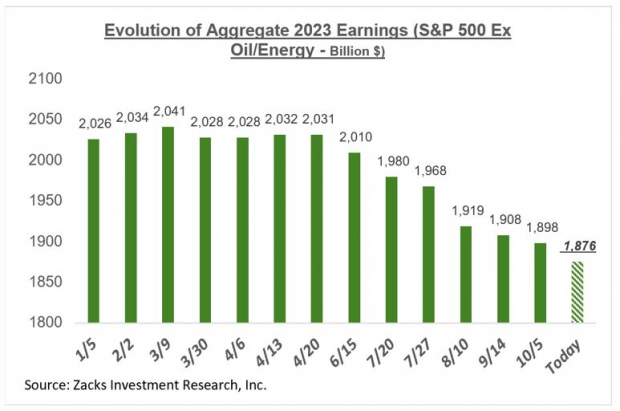

The chart under reveals how the anticipated mixture complete earnings for full-year 2023 have developed on an ex-Power foundation.

Picture Supply: Zacks Funding Analysis

As you possibly can see above, mixture S&P 500 earnings outdoors of the Power sector have declined -7.7% since mid-April, with double-digit proportion declines in Retail, Building, Client Discretionary, and Tech. Estimates have been coming down within the Industrial Merchandise, Medical and Transportation sectors as effectively.

The General Earnings Image

The chart under that gives a big-picture view of earnings on a quarterly foundation.

Picture Supply: Zacks Funding Analysis

The chart under reveals the general earnings image on an annual foundation, with the expansion momentum anticipated to proceed.

Picture Supply: Zacks Funding Analysis

Please observe {that a} massive a part of this 12 months’s progress is because of the robust momentum within the Power sector whose earnings are on monitor to develop +141.9%. Excluding this extraordinary Power sector contribution, earnings progress for the remainder of the index can be down -0.3%. This comparatively flat earnings image for this 12 months can be in-line with the financial floor actuality.

Earnings subsequent 12 months are anticipated to be up +5.6% as a complete and +7.2% excluding the Power sector. This magnitude of progress can hardly be referred to as out-of-sync with a flat and even modestly down financial progress outlook. Don’t neglect that headline GDP progress numbers are in actual or inflation-adjusted phrases whereas S&P 500 earnings mentioned right here are usually not.

As talked about earlier, 2023 mixture earnings estimates on an ex-Power foundation are already down -7.7% since mid-April. Maybe we see a bit extra downward changes to estimates over the approaching weeks, after we’ve seen Q3 outcomes. However we’ve nonetheless already coated some floor in taking estimates to a good or applicable degree.

That is notably so if no matter financial downturn lies forward proves to be extra of the backyard selection reasonably than the final two such occasions. Recency bias forces us to make use of the final two financial downturns, which have been additionally among the many nastiest in current historical past, as our reference factors. However we must be cautious in opposition to that pure tendency because the economic system’s foundations at current stay unusually robust.

7 Greatest Shares for the Subsequent 30 Days

Simply launched: Consultants distill 7 elite shares from the present checklist of 220 Zacks Rank #1 Robust Buys. They deem these tickers “Most Seemingly for Early Value Pops.”

Since 1988, the complete checklist has overwhelmed the market greater than 2X over with a mean achieve of +24.8% per 12 months. So be sure you give these hand-picked 7 your instant consideration. See them now >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

United Airlines Holdings Inc (UAL): Free Stock Analysis Report

Procter & Gamble Company The (PG): Free Stock Analysis Report

J.B. Hunt Transport Services, Inc. (JBHT): Free Stock Analysis Report

General Mills, Inc. (GIS): Free Stock Analysis Report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the creator and don’t essentially replicate these of Nasdaq, Inc.